Every second, consumers in Asia, the Americas, and Europe are completing transactions by pointing their smartphone cameras at a small square of black-and-white pixels. QR code payments processed $3 trillion in annual transaction volume in 2025 — and that number is accelerating fast. According to Juniper Research, QR payment values will exceed $8 trillion by 2029, representing a 50% surge in just four years. Whether you run a restaurant, a retail store, or a global enterprise, understanding how scan-to-pay works — and how to deploy it effectively — is no longer optional. This guide covers everything businesses need to know about QR code payments in 2026.

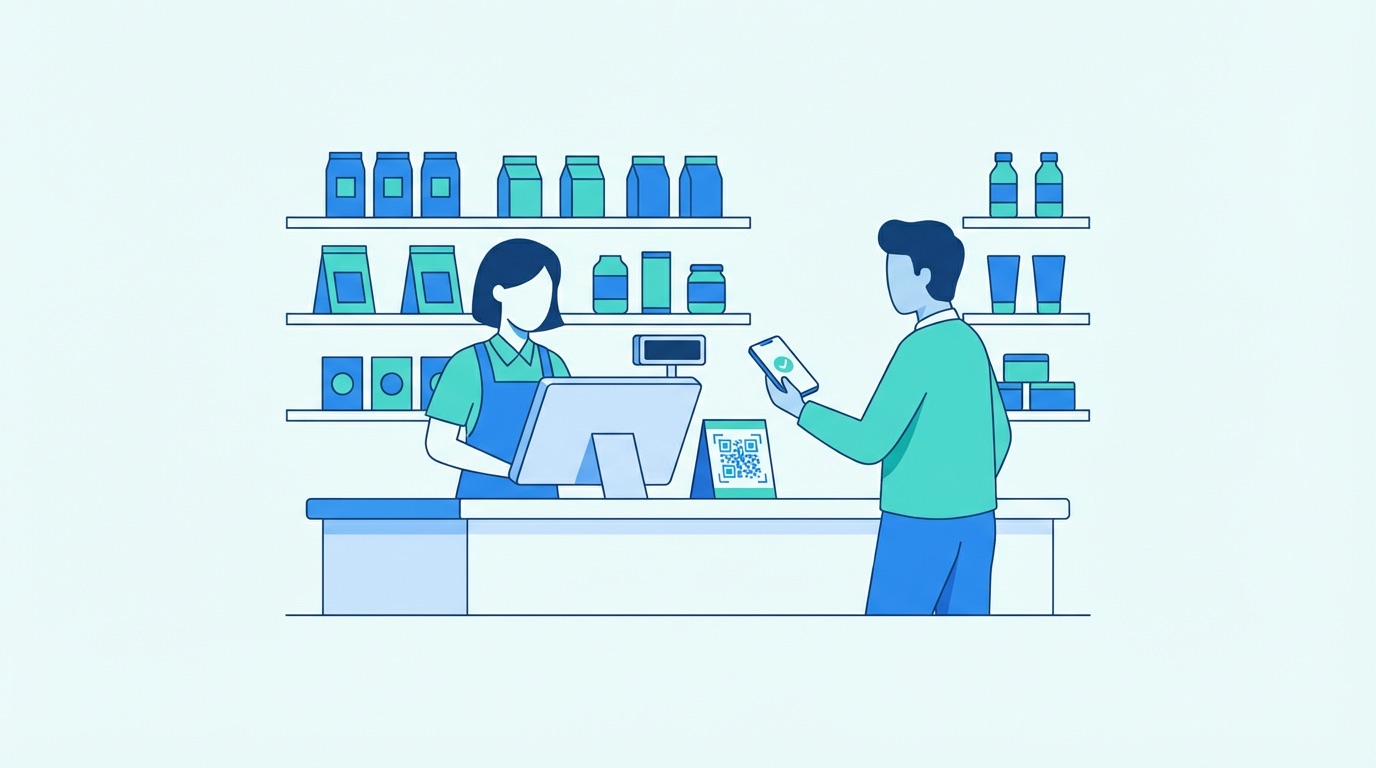

A QR code payment is a contactless transaction completed when a customer scans a merchant's QR code with their smartphone. Instead of swiping a card, tapping an NFC terminal, or handling cash, the customer opens a payment app or their phone's camera, scans the displayed code, and confirms the payment — all within seconds.

QR code payments come in two fundamental forms:

Both models are enabled by dynamic and static QR codes — though dynamic codes offer significant advantages for payment contexts, including the ability to update linked content, set expiry windows, and track scan analytics in real time. For a full breakdown of code types, see our guide to what QR codes are and how they work.

The user experience of QR code payments is deceptively simple. Behind a two-second scan lies a well-orchestrated sequence of data exchange, authentication, and settlement.

QR codes can encode merchant IDs, product-level data, loyalty points triggers, and UTM tracking parameters alongside payment information — making them significantly more versatile than standard NFC card terminals. For businesses looking to connect their QR payments to broader marketing analytics, the complete guide to QR code tracking and analytics explains how to build a measurement framework from the ground up.

The growth trajectory of QR code payments is one of the most compelling stories in global fintech. Here are the headline figures every business leader needs to know:

These numbers reflect a structural shift in how commerce is conducted — not a temporary post-pandemic trend. The convergence of smartphone ubiquity, real-time payment rails, and merchant simplicity is driving QR payments into every corner of the global economy. For a broader view of QR code adoption across all applications, the QR code statistics report for 2026 provides a comprehensive benchmark.

QR code payment adoption is not evenly distributed. Understanding which regions lead — and why — provides crucial context for businesses operating internationally or planning to scale across borders.

China processes over $5.5 trillion in QR code transactions, with consumers scanning codes 10–15 times daily as part of everyday life. WeChat Pay and Alipay have built ecosystems where QR codes have effectively replaced cash and cards for most transactions. Both platforms have now expanded to 20+ countries through international partnerships, bringing scan-to-pay to Chinese tourists and merchants worldwide.

India represents the fastest-growing QR payment market, with a 550% increase in adoption and 9 million+ merchants now accepting UPI (Unified Payments Interface) QR payments. The government-backed UPI infrastructure processes hundreds of millions of transactions daily, demonstrating what a unified national QR standard can achieve at scale.

The United States accounts for 43.9% of global QR code scans — more than any other country by scan volume — though payment adoption lags behind Asia. The shift is accelerating as Venmo, PayPal, Cash App, and bank apps have all integrated QR payment capabilities for both consumer-to-merchant and peer-to-peer transactions.

Brazil's PIX real-time payment system has enrolled 175 million users, becoming one of the world's most successful instant payment platforms. Latin America is now growing faster than Europe in QR payment adoption, driven by mobile-first populations and high unbanked rates that QR payments help serve through digital wallets.

Europe's QR payment landscape is maturing through standardization initiatives. The European Payments Council's SEPA Credit Transfer QR code standards are enabling cross-border interoperability. While NFC contactless has historically dominated, QR codes are gaining traction in restaurants, retail, and e-commerce checkout flows as merchants recognize the zero-hardware setup advantage.

Setting up QR code payments is substantially simpler and more affordable than deploying NFC terminals — typically requiring no specialist hardware and minimal technical integration. Here is a practical step-by-step framework:

Select a QR payment solution compatible with your existing banking and POS infrastructure. Options range from major processors (Stripe, Square, PayPal) to bank-native QR payment programs and regional fintech providers. Evaluate on: transaction fees, supported digital wallets, settlement speed, fraud protection, and customer support.

Your payment provider will supply a merchant QR code linked to your account. For static codes (fixed payment link), a single printed code works for low-volume or single-location businesses. For dynamic transaction-specific codes (where each order generates a unique code with the exact amount), you will need POS integration or a QR code generator with API capabilities.

For businesses managing multiple locations, campaigns, or payment touchpoints, a professional QR code platform like Supercode enables bulk code creation, design customization, and centralized analytics tracking — making large-scale QR payment deployment manageable from a single dashboard. See our guide to bulk QR code generation for enterprise workflows.

Placement matters enormously for scan rates. Best-practice positions include:

Before going live, test the entire payment flow end-to-end on multiple devices (iOS and Android) and payment apps. After launch, monitor transaction completion rates, average order values, and any abandoned scan events — all available through a dynamic QR code analytics dashboard.

No industry has embraced QR code payments more enthusiastically than food service. The convergence of digital menu adoption (accelerated by the pandemic), faster table turnover demands, and contactless payment preferences has made QR payments a permanent fixture in modern dining.

Key benefits for restaurant operators include:

For a comprehensive operational guide covering digital menus, ordering systems, and payment integration, see our dedicated resource on QR codes for restaurants. For material-specific placement best practices, the QR codes for menus page provides detailed guidance.

Retail is the second-largest adopter of QR code payments globally, and the use cases extend well beyond simple checkout. Smart retailers are deploying QR payments across the entire customer journey — from discovery to purchase to post-sale loyalty.

High-impact retail applications include:

The connection between QR code payments and broader sales growth is well-documented. Our analysis of how QR codes increase sales documents 10 proven strategies retail businesses are using in 2026, including point-of-interest promotions, mobile commerce acceleration, and dynamic personalization. For the finance and payments industry specifically, see QR codes for finance and insurance.

Both QR codes and NFC (Near Field Communication, the technology behind contactless card tapping) are mainstream payment methods in 2026. Understanding their respective strengths helps businesses make the right choice — or deploy both in combination.

QR codes have a clear advantage here. Printing or displaying a QR code requires virtually zero specialist hardware — a laminated card or a screen is sufficient. NFC terminals cost anywhere from $50 to $500+ per device, require PCI-compliant certification, and need ongoing maintenance. For small businesses, pop-up vendors, and businesses in emerging markets, QR codes dramatically lower the barrier to accepting digital payments.

NFC payments are generally faster at the point of terminal interaction — a tap takes under a second. QR code payments require the customer to open their camera or app, point, and confirm — adding 5–15 seconds to the process. For high-volume, queue-sensitive environments like coffee shops at peak hours, this can matter.

QR codes win decisively on versatility. A QR code can be placed on a poster, a receipt, a product label, a shop window, or a website — anywhere a physical or digital surface exists. NFC requires proximity hardware and is limited to point-of-sale contexts. QR codes also encode far more information than a standard NFC payment tap, enabling rich post-payment journeys (loyalty enrollment, review requests, upsell offers).

Both technologies have security considerations. NFC uses encrypted secure elements that offer strong protection against interception. QR codes are susceptible to "quishing" attacks — where fraudsters replace legitimate codes with malicious ones. However, dynamic QR codes (which rotate URLs and can be deactivated remotely) substantially mitigate this risk. For a full security analysis, see our comprehensive guide on QR code safety in 2026.

The verdict: For most businesses, the right answer is both — NFC terminals at primary POS for speed, QR codes everywhere else for flexibility, marketing integration, and zero-hardware reach.

Static QR codes — where the encoded data is fixed at creation — can work for permanent payment links, but dynamic QR codes are transforming what's possible in payment contexts. A dynamic QR code stores only a short redirect URL in the code itself; the destination URL can be updated at any time without reprinting the code.

For payment applications, dynamic codes unlock capabilities that static codes simply cannot offer:

For businesses deploying QR codes at scale — across multiple locations, products, or campaigns — Supercode's QR code generator provides dynamic code creation with real-time analytics, bulk generation, and branded code design from a single platform.

Security is the most common concern businesses raise when evaluating QR code payments. The threat is real but manageable with the right practices.

Quishing (QR code phishing) involves replacing a legitimate QR payment code with a fraudulent one that directs customers to a fake payment page to steal card details. Between April 2024 and April 2025, UK police recorded 784 quishing incidents resulting in £3.5 million in losses. The threat is rising in parallel with QR payment adoption globally.

For customers, the best protection is verifying the URL preview before confirming payment and using banking apps with built-in fraud detection rather than entering card details manually. For a deep dive into all QR code security vectors, our guide on QR code safety and quishing covers enterprise defense frameworks in detail.

QR code payments generate rich behavioral data that most businesses leave on the table. With the right tracking infrastructure, every scan becomes a data point that can improve conversion rates, customer experience, and marketing ROI.

Add UTM parameters to the payment landing URLs embedded in your QR codes to connect transaction data with Google Analytics 4 campaigns. This closes the attribution loop between a physical placement (a restaurant table card, a retail shelf sticker) and a verified transaction — the holy grail of omnichannel attribution. For a step-by-step guide, see our resource on QR code tracking and analytics.

QR payments also create the ideal moment to capture zero-party and first-party data. Post-payment QR journeys — asking customers to confirm their email for a receipt, enroll in loyalty, or leave a review — can achieve 40–60% completion rates versus 15–25% for follow-up emails. For strategies to maximize post-payment customer engagement, see our guide to QR code customer feedback.

The QR code trends for 2026 confirms that QR-driven first-party data collection is now a primary strategic driver for enterprises, with 95% of businesses using QR codes to gather customer data.

Yes, when used with reputable payment providers and legitimate merchant codes. Customers should verify the URL preview before confirming payment and use their banking or wallet app rather than entering card details manually. Dynamic QR codes from verified merchants are significantly more secure than static codes, as they can be deactivated if compromised.

In most markets, no. Modern smartphones on iOS and Android can scan QR codes directly through the built-in camera app, which opens the payment link in the default browser or redirects to a supported payment app. Some QR payment systems (WeChat Pay, Alipay) do require their dedicated apps, but universal payment QR codes work with standard camera functionality.

Costs vary by payment provider. Most charge a transaction fee (typically 1.5%–3% per transaction, comparable to card processing fees) but have no hardware costs, unlike NFC terminal deployments. Generating and managing QR codes through a professional platform covers code design, analytics, and dynamic code management.

Partially. The QR code itself can be displayed offline. However, completing a payment transaction requires an internet connection on the customer's device to transmit payment instructions to the processor. In low-connectivity environments, some payment systems support offline transaction queuing, settling when connectivity is restored.

A static QR payment code encodes a fixed payment URL that cannot be changed once printed. A dynamic QR code stores a short redirect URL that can be updated, tracked, and deactivated at any time. For payment contexts, dynamic codes are strongly preferred — they enable transaction-specific amounts, real-time analytics, expiry controls, and instant deactivation if compromised.

Yes, and many businesses do exactly this. A dynamic URL QR code can link to a landing page that serves both a payment function and marketing content — such as a product page that includes a purchase button, loyalty enrollment, and brand storytelling. Using a QR code platform with campaign management allows you to A/B test different post-scan destinations without reprinting codes. Learn more about QR code marketing strategies to maximize the value of every scan.

Restaurants and food service lead adoption, followed closely by retail, hospitality, transportation, and financial services. The fastest-growing sectors in 2026 are healthcare (contactless billing), events and ticketing, and luxury goods (authentication + payment bundled in one scan). For a full breakdown of industry-specific QR code strategies, explore the QR code industries hub.

QR code payments represent one of the most significant shifts in global commerce infrastructure since the introduction of contactless cards. With transaction values heading toward $8 trillion by 2029, a market growing at nearly 20% annually, and adoption spanning from street food vendors in Mumbai to luxury boutiques in Paris, the question for most businesses is no longer whether to implement scan-to-pay — it's how fast.

The businesses winning with QR payments in 2026 are those treating each code not just as a payment method, but as a dynamic data collection, loyalty, and marketing touchpoint — connecting the physical moment of purchase to a rich post-transaction customer relationship.

Ready to deploy professional QR code payments with analytics, dynamic codes, and branded design? Start your free trial with Supercode today and create your first payment QR code in under two minutes.